The Federal Reserve is balancing a split economy

Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

- 2Q GDP data was less impressive than the headline number suggested

- We expect the Fed to respond to slower growth in 2H25 by cutting rates

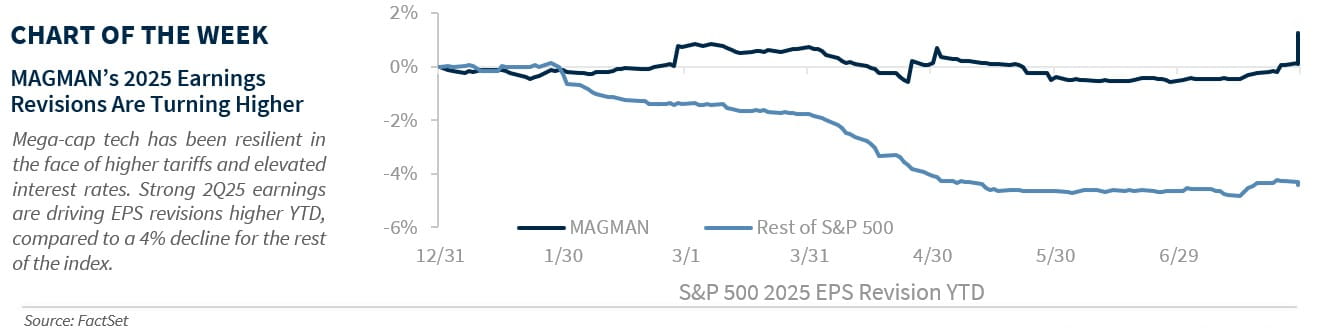

- Excluding MAGMAN*, 2Q earnings are tracking to muted growth

The Great Divergence: Tech’s Rise and the Economy’s Strain. This week brought a wave of headlines for investors to digest – on both the macro and micro fronts. On the economic side, growth bounced back sharply in 2Q, with GDP rising at a 3% annualized pace (versus -0.5% in 1Q). But beneath that strong headline, there are signs that underlying demand is starting to cool. The Fed seems to agree. While it acknowledged the downside risks to growth, policymakers chose to keep rates steady, largely because they’re more concerned about the inflationary impact of looming tariffs. On the corporate side, tech earnings were the standout performer. Several major tech names posted exceptionally strong results, underscoring the growing divide between the Technology sector and the rest of the market. These mega-cap tech companies haven’t just powered the S&P 500’s rebound and pushed the NASDAQ to new highs since the post-Liberation Day lows – they’ve also helped offset the drag from tariffs and tight Fed policy through massive capital spending.

- ‘Core’ economic growth is slowing, despite The 2Q GDP rebound | 2Q growth rebounded sharply, rising at a 3% annualized pace. But a closer look reveals some cracks beneath the surface. A big boost came from a swing in net exports—largely due to tariff front-running in 1Q—while personal consumption remained soft, growing just 1.4%. The first half of 2025 marked the weakest two-quarter stretch for consumer spending growth (+0.5%) since 3Q20. Real-time data shows consumers are still spending on services like travel and dining, but goods spending is lagging as tariffs begin to bite. Business investment also tells a split story: residential investment declined for a second straight quarter due to high rates, while AI-related capex remains strong. One key measure of underlying demand—final sales to private domestic purchasers—slowed to just 1.2%, the weakest since late 2022. With growth showing signs of stalling, the labor market will be critical. Today’s jobs report showed just 73k new jobs added, alongside significant downward revisions to prior months—echoing forward-looking indicators that point to further cooling ahead. We continue to expect job growth to remain weak into year end.

- The Fed is balancing a bifurcated economy | The July FOMC meeting was largely uneventful. Despite signs that the economy is slowing, officials kept interest rates steady at 4.25%–4.50%. Two Fed Governors, Waller and Bowman, dissented as they wanted a small rate cut, pointing to a softening job market. But most members preferred to hold off until they get a clearer read on how new tariffs might affect inflation. The Fed is walking a tightrope. Inflation is still stubborn, but the economy is clearly split. Lower-income households are feeling the pinch from high prices and borrowing costs, while wealthier Americans and big corporations have largely weathered the storm. Large companies, especially the mega-cap tech companies, are still spending thanks to strong earnings growth and substantial cash reserves. Meanwhile, small businesses and the housing market are struggling under the weight of high interest rates—borrowing costs are near 9% for small firms, and mortgage rates are hovering around 7%. Given these pressures, we think the Fed will likely start cutting rates later this year as growth continues to cool.

- Narrow leadership is driving 2Q25 earnings | With ~60% of the S&P 500 market cap having reported so far, nearly 81% of companies are beating their EPS estimates—well above the historical average of 75% and the highest beat rate since 3Q23. However, much like the broader economy, the story is more nuanced beneath the surface. While S&P 500 earnings are on track to rise for the eighth straight quarter, the YoY growth rate (+5.6%) is the slowest since 4Q23.

- Tech remains the clear standout—Mega-cap tech continues to show strength, with the consensus expecting MAGMAN earnings to rise 21% YoY. So far, five of the six have reported—Microsoft, Apple, Alphabet, Meta, and Amazon—and they’ve beaten expectations by an average of 14%, driven by growing AI adoption and strong cloud demand. Notably, these companies are ramping up their investment plans. As data center demand continues to outpace supply, they’ve raised their capital spending guidance for both 2025 and 2026. This reinforces just how resilient the mega caps have been, even in the face of higher tariffs and elevated interest rates.

- Rest of index remains subdued—Outside of mega-cap tech, earnings results have been more mixed. Excluding MAGMAN, S&P 500 earnings are on track to grow just 4% YoY in the second quarter. There are bright spots—banks and credit card companies continue to point to solid consumer spending. But companies tied to goods and manufacturing are feeling the strain from tariffs. Stanley Black & Decker, Whirlpool, and UPS have all flagged softer consumer demand. Meanwhile, firms like Procter & Gamble, Hershey’s, and Amazon are facing pressure from rising input costs, which is likely to weigh on their margins and profitability in 2H25.

This divergence is showing up in full-year earnings revisions. For 2025, estimates for mega-cap tech have been revised higher, into positive territory, while the rest of the index has seen a 4% decline. We continue to favor the Tech sector, along with Industrials – which play a key role in supporting the ongoing AI buildout.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee, and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success. Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.